Reductionist "Reductions" Beware - LETS Improve accounting to Bolster Book and Claim Acceptance

- A blog post by the Methods, Standards, & Assurance Team at Smart Freight Centre

A Short Summary:

"Book and claim systems help jumpstart logistics decarbonization. Altruism only gets us so far. An organization's value chain-based investments via book and claim must count. Accounting and reporting standards for greenhouse gas emissions are under review, in transportation and beyond, and don't allow for carbon credits. "Netting," or subtracting "reductions". At the same time, transportation accounting has a standard: ISO 14083. If organizations get a little nerdy today, they set the ecosystem up for success tomorrow. When booking or claiming, accounting for the lower emission profile - not the "reduction" - is more consistent with standard logistics accounting, aligns all users of a "market-based" approach, and such standard accounting and alignment might increase the chance book and claim is approved by key reporting and target bodies. End result = more decarbonization."

You’re sitting outside the CEO’s office, prepared to present your logistics decarbonization plan. You have 10 minutes to make the case, and you know two questions will come your way:

- How much is it going to cost?

- How much are we “reducing”?

You seek to green-light increased investment in sustainable fuels and services. You know this plan is critical in a climate crisis, will help your organization reach its net zero targets, and will ensure your end-of-year greenhouse gas (GHG) emissions inventory remains low. You know 85% of consumers prioritize sustainable choices and the consensus among 97% of scientists on human-caused global warming all but demands this plan’s approval. However, you also know the sustainable option is still more expensive than traditional fossil transportation, customer wallets are tight, and finally - and most fun - you know that your plan depends on a flexible, traceable chain of custody model called "book and claim". (1)

You follow all the rules, but GHG emissions accounting can be wonky, and current gray areas in “approval” for market-based approaches such as book and claim inject just enough risk to potentially scare your CEO. Also, you and your colleagues realize, like last month, your 10 minutes in this “boss” check-in will likely get cut to 5!

This is a story about the importance of your work (thank you!), about caution and intentionality when leveraging a market-based approach, and about how to deliver real, effective and cost-efficient “reductions” to your CEO while also respecting accounting rules that might even increase the chances this very approach is approved.

Said another way, “netting”, carbon credits, and selling “reductions” aren’t allowed inside corporate inventories by the Greenhouse Gas Protocol (GHGP), today, nor can they be applied towards the Science-Based Targets initiative’s (SBTi) net-zero commitments. High quality book and claim, however, may be different. Recognizing the need to jumpstart hard-to-abate sector decarbonization, these organizations are currently reviewing the practice and currently provide cautious and mixed guidance on market-based, in-value-chain procurement models for transportation. Thus, while book and claim systems remain under study, it’s more important than ever to be diligent when integrating book and claim procurement into accounting and reporting - for the sake of your operations, your customer’s low-emission claim, and the environment.

There is a tonne of emphasis on differences between traditional fossil freight and low emission transportation alternatives. That being said, taking a few minutes to focus on GHG emissions accounting methodology when using ‘book and claim’ systems is crucial when a whole community seeks approval for these in-value-chain tools to “count” in inventories and towards decarbonization target commitments. We’re counting on you.

So, what are we doing when booking and claiming? And what should we have in mind when we feel the urge to offer “reductions” and keep things simple for our CEOs and customers?

Using Old Systems, Building New Ones

Leading organizations are making monumental investments in key decarbonization pathways and sticking their necks out in a high-pressure, “greenwashing”-conscious world. Their attention to emission accounting rules and “claims” today just might make or break the community’s ability to deploy high quality market-based products tomorrow—products that make very real, very needed environmental impact and send a demand signal that spurs increased supply of green alternatives.

Take the example of an airline wishing to purchase SAF (or a carrier in any transport mode). If SAF volumes were available at the gate, they could purchase and simply uplift this revolutionary fuel. They would receive documentation corroborating this purchase, its physical delivery, and account for transportation activity using its “attributes” - i.e., the low emission profile - commonly up to 90% less emissions-intense than traditional fossil jet fuel.

But SAF is produced at only 40 facilities globally today, makes up less than 0.1% of total jet fuel consumed, and new supply isn’t matching expanding demand. This means that SAF providers still must share existing infrastructure - a mixed hydrant system or fuel farm - given it is currently cost-prohibitive to create dedicated delivery infrastructure. Biomethane delivery via a common pipeline leverages the same concept. To facilitate delivery of a mixed-molecule fuel, with associated environmental attributes and documentation, stakeholders use a mass balance chain of custody model (2). Now, who gets to account for the low emission SAF in the mixed supply?

Given all jet fuels are certified to the same - or similar - operational standards, when an air carrier connects to supply via a pipeline or fuel farm and purchases SAF, mass balance rules let the carrier claim the “good stuff” is on their plane even though they’re technically receiving the same blend as their neighbor. The system depends on documentation and rigor. Fuel providers and users recognize the need to share infrastructure and have used this methodology for ages to avoid unnecessary costs. Tried and true. Approved and used in all transport modes and approved for claims in the carrier’s GHGP-based emission inventory and towards SBTi targets.

This Book & Claim logic and rulebook were adopted in the electricity sector, and high-quality application is allowed for accounting and reporting emissions related to the supply of electricity (scope 2) by GHGP and SBTi

With a ‘book and claim’ chain of custody model, the intellectual and molecular leap grows. Book and claim can be highly traceable but embraces physical separation. The value chain can follow the fuel delivery to a wing in Singapore, but the sustainable attribute’s documentation might be delivered to Panama City where a carrier claims the SAF’s lower emission profile. When there is no pure or mixed option physically available, the carrier receives documentation corroborating their procurement by leveraging an audited, traceable book and claim system such as a “registry”. This helps the carrier procure the solution “virtually”, secure their desired sustainability and emission profile, and make a unique claim in their GHG inventory. All actors recognize this SAF is not physically uplifted in Panama City. The low emission fuel molecules will be physically burned in a different location within the aviation value chain, and careful system setup mitigates double-counting risk.

Mother earth doesn’t care where the SAF is burned. So long as we continue flying, its booked-and-claimed, lower emission profile benefits all who fight climate change and environmental degradation while keeping costs palatable for airline carriers and customers. This book and claim logic and rulebook were adopted in the electricity sector, and high-quality application is allowed for accounting and reporting emissions related to the supply of electricity (scope 2) by GHGP and SBTi. By applying the same logic to the heavy transportation industry, and applying it well, we can implement innovative transportation solutions more cost-effectively, help meet the aviation sector’s net zero goal by 2050, and repeat the feat in all transport modes.

To do this, we need to get a little nerdy with emissions accounting. Altruism will only take us so far. We want this carrier - need this carrier! - to be allowed to claim the lower emission profile resulting from their high-quality book and claim-based fuel procurement. The same logic applies to a shipper (i.e., cargo owner) who seeks a book and claim-based transportation service from a carrier. They may have no other option. Users and providers have a joint responsibility to bear and share costs, but they must be able to account for such procurement in their corporate inventories to justify the premium. Without such a jumpstart, we simply cannot produce enough SAF, sustainable marine fuel (SMF), or any low emission transportation solution and deliver it everywhere, physically, in this decisive decade.

The “Green Visor” of Emissions Accounting

Now the fun part. Getting out calculators, putting on “green” accounting visors, and reporting low emission transportation solutions and services from book and claim in a high integrity manner will increase industry alignment, connect supply to demand, and enable first movers to buy more, produce more, and offer more sustainable alternatives.

We've all seen someone's eyes glaze over with "accounting" talk, documentation, "registry", rigamarole, or anything that sounds like tax season

We’ve all seen eyes glaze over with accounting talk, documentation, registry rigamarole, or anything that sounds like tax season. This is one reason it can be attractive to try and sell the “reduction”: it’s easy for the lay person to understand. However, for those trying to make it easier for customers to purchase and claim the green solution, we need to enable our green-visored accounting friends to do what they do best - track, trace, claim, and report for low emission solutions and services in the market based value chain just as if the solutions and services had been physically consumed. This is not achieved by simply counting reductions but rather by a normative, inventory approach to book and claim.

Inventory accounting is used to account for total emissions associated with an organization’s activities - e.g., a corporate GHG inventory. In the above example, the airline procures fuel and attributes within a system that is knowingly disconnected from physical supply, yet highly traceable, enabling its inclusion in an inventory. This is also called attributional accounting, and in transportation, the emission profile’s attributes are co-reported in respective corporate inventories as the operator’s scope 1 and energy-related scope 3 emissions, and the supply chain actors account for the same emission profile in their transportation-related scope 3 reporting.

This is different from a project- or intervention-based accounting approach, which “estimates the impacts or changes in GHG emissions resulting from specific projects, actions, or interventions relative to a counterfactual baseline scenario.”This approach is also called consequential accounting, and one of its most common applications is by organizations that want to “reduce” environmental impact from activities via carbon offsets.

With an offset, the carrier may choose a project to “compensate” for high transportation emissions, for example, forest-based offsets to try and sequester their recently-emitted carbon. The carrier reports transportation emissions in their inventory with appropriate values and reports offsets outside of their inventory as a (-) subtraction. Unlike transportation’s inventory accounting described above, use of an offset entails that no other player in the value chain benefits from offset.

However, two principal issues arise with impact-based offsets. First, in the case of the aviation example, such out-of-value chain options do not address aviation emissions. The same principle applies for each mode. Second, as mentioned above, they are not allowed by key reporting and targets bodies such as GHGP and SBTi.

How then, do we get “reductions” today? How can the air carrier account for the booked-and-claimed SAF fairly, today, while avoiding the reductionist “reduction” that seems easy to subtract and often looks and feels like an offset?

Ride the Horse That Got Us Here - Accounting for the ‘Thing’ You Normally Procure

Now, let’s return to the airline who wishes to keep their in-value chain emissions low by procuring SAF via book and claim. The carrier has no physical, sustainable fuel available through its existing partner network and selects certified SAF via a book and claim system. A robust yet simple system of auditors and interoperable registries exists to ensure no other carrier procures the same solution attributes. The carrier conducts transportation activity using the lower emission profile of their claimed SAF, and all related parties appropriately report the GHG emissions in their inventory. How should they do that?

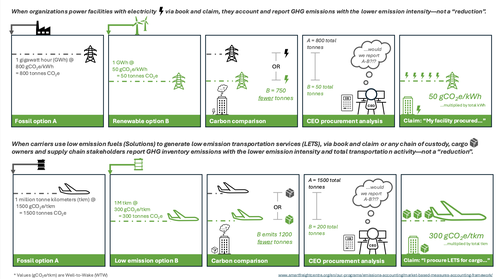

Rather than create a new system of accounting, we suggest that a high-quality market-based approach in transportation follow the same principles as the high-quality physical approach hammered out by the industry over the last 10+ years, leading to ISO 14083. Solution providers provide energy (e.g., fuels) to carriers, passing along the same data as if they’d used the physical fuel. Carriers consume these solutions while producing transportation activity for their LSPs and cargo owners (shippers), and the emissions profile of these services are communicated down the value chain by providing standard data on the amount of cargo moved + associated emissions—combining this data into a GHG emissions intensity using normative logistics units: e.g., grams of CO2e per tonne kilometer (g CO2e/tkm, or tonnes CO2e/TEU-km, /pkm, etc., as appropriate).

While it may be tempting to simply provide an organization a (-) negative value of tonnes of CO2e to subtract from their corporate inventory, this flirts with the project/impact/consequential accounting approach that is currently prohibited and risks confusion with standardized transportation accounting.

Today's CEO has their eyes to the future, cognisant of long-term trends and goals. They understand when diligence today can yield a better tomorrow

Imagine following normative inventory accounting for your fossil and low emission fuel—delivered by any chain of custody—and then being passed a “reduction”? Imagine a shipper who procures transportation services every day of the week… until they’re handed a new unit: liters of sustainable fuel? Tonnes of “neat” SAF? (i.e., pre-blending) These practices risk creating a mixed accounting atmosphere, limit book and claim to only the most sophisticated teams, and may signal to key observers that sector emissions could be counted incorrectly—greenwashed even—potentially limiting approval from key policymakers and observers for use of book and claim-procured decarbonization in inventories and toward targets.

But! - How Do We Get the CEO Her Reductions?!

The desire to ‘reduce’ year over year emissions and overall environmental impact is of paramount importance. Furthermore, it cannot be expected for every CEO to understand ISO 14083 accounting. Inventory-what? Consequential-what?

At the same time, CEOs do understand “approved” and “this claim won’t count without…”. They are busy handling every aspect of their organization’s operations and need the shorthand of “how much am I reducing” and “how much will it cost me”. Especially in an ‘internal pricing system’, the sustainable options will be compared between different carbon abatement costs and risks. Today’s CEO has their eyes to the future, cognizant of long-term trends and goals, the non-monetary value of sustainable investments, and they also understand when diligence today can support a better tomorrow.

The “reduction is generally discussed in one of two places, depending whether your organization consumes fuel or consumes services, and both situations merit extra attention by community stakeholders.

First, we highly recommend providing the sustainability and emissions profile of a low emission solution to a fuel user as if they had actually received the physical fuel. Yes, this may be via digital documentation, but such documentation still provides the necessary data to account for the low emission solution. The physical fuel pump may not have the actual low emission solution. The experienced operator is aware that the solution provider’s salesperson might offer the book-and-claim ‘fuel pump’ procurement option as “reductions” [G6] because this sounds simple and communicates one of the integral components the sustainability manager seeks: lower GHG emissions in their inventory. However, the operator will also ask for the full sustainability and emission profile of the solution.

The traditional choice, fossil jet fuel, would implicate higher emissions—let’s say, 10 tonnes of CO2e (10t). Via any chain of custody, when a solution provider hands a carrier SAF with a lower emissions profile—let’s say 2t—they’re handing the carrier a 2t documentation, not the equation “10t - 2t = 8t” nor are they handing the carrier a -8t documentation of reductions to subtract. In book and claim procurement, the accounting-conscious operator will ask for full documentation and attribute data while accounting for the sustainable solution with the 2t, as if they’d received the physical SAF. This simplifies calculation for downstream entities as well!

As noted, one may still say “reductions” to translate this to the CEO and help them justify the extra investment, but to facilitate the green-visored accountant’s work and industry alignment, it’s highly recommended to provide the complete data of the solution profile and account following the standard transportation toolset as closely as possible.

This is one reason that solutions are often best understood by carriers—organizations that operate transportation assets and procure and use fuels to conduct transportation activity. Similar to physical fuel procurement, book and claim procurement includes, at minimum: the quantity (volume, mass, and/or energy content); the GHG emissions profile; and feedstock data. Some advanced cargo owners, for example, do procure solution profiles, but this practice is not recommended for novice organizations (4).

This is the most-common situation where we see book and claim system participants attracted to the shortcut term “reduction”.

The hurry is understandable, and the desire to “reduce” year over year emissions and impact is real. However, when booking and claiming, it’s worth taking a moment to provide and/or procure the nerdy product—the LETS—that aligns with attributes of all other traditional (often fossil-based), physical transportation as reported in their operations and accounted for in their GHG inventory. The LETS includes five components: mode of transportation, amount of transportation (e.g., tkm), GHG emissions intensity (e.g., g CO2e/tkm), total GHG emissions, and the transportation operation category (TOC) where possible (TOCs are groupings that help organizations take a systematic approach to a complex set of total transportation activities).

Cargo owners make up approximately 80% of all SBTi target setters. Thus, it’s especiallyimportant for these shippers to understand how to procure the product that’s aligned with normative transportation service accounting. Shippers are sophisticated, but their primary function is not transportation itself. It is a means to an end: moving goods to market. They’re results-oriented and are, yes, admittedly often thinking one step beyond the “lower emission profile” transportation to consider another objective: a shiny, super-small # in their final GHG inventory for public and investor consumption. This urge, together with offset familiarity, means that “reductions” sell but can easily cause confusion when accounting and reporting.

Salesfolk higher in the value chain—solution providers, carriers, and LSPs—know that some shippers want to participate in the low carbon economy anyhow, anyway, and it can be tempting to keep the offer too simple. It’s not malicious. Anecdotally, this practice is often due to the necessary nerdiness mentioned above—transportation emissions accounting can induce headaches, mirroring the complex logistics ecosystem itself. However, with great power comes great responsibility.

We urge such actors to take the extra time to set their clients up for success and use standard transportation units, high quality data, and report the lower emissions profiles of booked and claimed solutions or services as close as possible to the standard transportation supply- and value-chain methodology. The shipper’s procured and claimed LETS has a lower emission profile and is the “reduction” the CEO wants to see.

Final Words of Wisdom Before Your Meeting - “Don’t Worry, I’m an Expert”

The hurry is understandable, and the desire to "reduce" year over year emissions and impact is real. However, when booking and claiming, it's worth taking a moment and procuring the nerdy product - the LETS

You’ve got this! When preparing for the CEO’s office, remember to arrive early. Refine the message. Hone the pitch. You’ve worked hard to get here. And when you end up with only 5 minutes, don’t fret if you need to use the shorthand term “reductions” to sell the vision. Again, understanding ISO 14083 accounting can be challenging, and that’s not their job today.

However, to help your leader steer the organization towards financial and environmental success, won’t they be pleased to know you’re using the logistics industry’s standard units? Won’t they be pleased to know you’re aligning your organization’s practices with the existing—and approved—methodology utilized in the electric sector and followed by leading organizations in the wider book and claim community?

From the bottom of our tree- and LETS-hugging hearts and green visors, we thank you for promoting low emission solutions and services and spurring transportation decarbonization. On behalf of advocates for high-quality market based procurement, we thank you for leading the way and showing organizations such as GHGP and SBTi that, even when procuring via book and claim, “we’ve got this!”

(1) Book and Claim: “Chain of custody model in which the administrative record flow does not necessarily connect to the physical flow of material or product throughout the supply chain.” See, ISO 22095.

(2) Mass Balance: “Chain of custody model in which materials or products with a set of specified characteristics are mixed according to defined criteria with materials or products without that set of characteristics.” See, ISO 22095.

(3) Registry: A tool to register and track the transfer of the characteristics of a Solution or LETS. (SFC MBM Specification

(4) Note: It’s worth noting that advanced transportation organizations that are not carriers and wouldn’t normally consume fuels (e.g., LSPs or Shippers), may also choose to procure solution profiles directly from a solution provider. This is one practice employed today while shippers aren’t seeing enough offerings of sustainable transportation, but it implicates some risk. They are assuming the responsibility of translating the units into their own inventory as if one of their carriers had utilized the fuel to move their goods. This requires specific expertise and is not recommended for novice organizations.